From compliance to opportunity: Transformative strategies for value creation

An intensified commitment to sustainability in Europe, driven mainly by the Paris climate agreement and EU taxonomy, has put the real estate industry under pressure to implement significant transformation. The recently revised Energy Performance of Buildings Directive (EPBD) and the Energy Efficiency Directive (EED) envisage a highly energy efficient and decarbonised building stock (a defacto zero-emission building stock) by 2050, and at least a 55% reduction in greenhouse gas emissions (compared to 1990) by 2030 (source). In response to these directives, the European Union has set a target of renovating 25% of the most energy-inefficient properties within its member states by 2033. Additionally, starting from 2030, all new builds must meet strict emission-free criteria with regard to both the manufacture and disposal of construction materials. Furthermore, the EU plans to phase out the use of fossil fuel-based heating by 2040 (source).

The regulatory framework in Switzerland is less developed, but the country has made a strong commitment to climate goals by adopting the Federal Council’s long-term climate strategy (2021) and passing the "Climate and Innovation Act" (2023), which established a net-zero target. Given the significant contribution of the real estate and construction sector to primary energy consumption (36%) and greenhouse gas emissions (37%), the sector has rightly been put under the spotlight by civil society and political decision-makers as they seek to reduce global carbon emissions and achieve the Paris Agreement’s 1.5-degree target by 2050. Decarbonisation must therefore be prioritised in the development, construction, and management of real estate.

This evolving regulatory framework is particularly critical for asset managers and banks, because properties that fail to meet new standards increasingly risk becoming 'stranded assets' (reduced fungibility, style/risk shift). To prevent this happening, owners often have to allocate significant funds to renovation in order to meet new energy and social standards, and avoid “brown discounts”. We believe that ESG-conformity will soon be “the new normal”, meaning that assets that fail to meet a certain rating will be discounted - rather than those that fulfil ESG requirements attracting a premium. Taking the German office market as example, up to 69% (€ 303 bn) of all Top-7 office properties are at risk of becoming stranded, according to Colliers.

«The push towards a sustainable building stock is not just a compliance exercise but a strategic opportunity to redefine Real Estate portfolio management.»

Armin Hafner, CAIA

Team Lead Real Estate Investment

Stranded assets within investment styles

Practitioners and academics usually classify real estate properties according to their risk-return profiles, using the terms ‘core’, ‘value-add’ and ‘opportunistic’ as proxies for the level of predictability of future cash-flows and value development:

- Core properties are those that achieve a significant portion of their returns from current income and are characterised by rather low volatility and often lower levels of leverage. They are thus assumed to be the most liquid class even in challenging market environments.

- Value-add and to a certain degree opportunistic properties are those that are in transition and which may or may not generate active cashflows. Future cash flows are not yet stabilised owing to current conditions and are characterised by a certain (substantial) level of uncertainty. Compared to core assets, value-add assets tend to generate less current income and rely more on (future) value appreciation as a component of total returns.

In general, owners aim to improve asset characteristics by employing several strategies including physical changes/capex, repositioning, or a change in tenant mix. These approaches require active management. Successful implementation and outcome thus rely heavily on the skillset of the manager or mandated third party and their ability to successfully identify and execute measures that add true value.

UBS defines a stranded asset as one “that loses its value earlier than expected, normally because of changing economic structures […] turning previously secure investments into liabilities”. The author would add ‘regulatory structures’ to this definition and locate such assets between core and value-add, with a tendency to value-add; though a differentiation must be made according to the property type and its main characteristics (e.g. residential vs. office).

Institutionally held residential properties facing the threat of stranding in Germany or Switzerland are still cash generating, predominantly show low levels of leverage and currently enjoy small or tolerable vacancy rates in metropolitan areas. However, they could still face a short to mid-term risk of devaluation, substantial statutory obligations to make energy-efficient renovations, and reduced fungibility (up to the point of not being sellable or rentable at economically feasible prices).

In the office property sector, the risk of (future) vacancies is much higher and resilience is much lower, so there is a significantly greater overall risk of becoming stranded or even obsolete. Colliers refers to the “stranding-asset-point” – the point where there is an “unexpected” decrease in income or even a total loss of value (source).

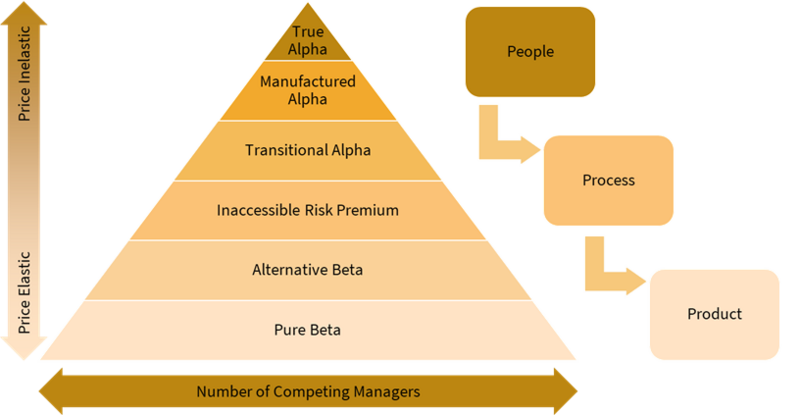

A brief introduction to alpha

Alpha can be described as an excess (or abnormal) return on an investment relative to its benchmark as the result of active investing, which cannot be described by known factors but is due to skill or luck. If an abnormal return persists over time (abnormal return persistence) it might be an indicator of skill rather than luck.

Within a portfolio, certain alternative assets can act as alpha drivers. In general, drivers of returns include investments, products and strategies that generate the portfolio’s risk and return; these are commonly divided into beta and alpha drivers. Alpha drivers are defined by the investment strategy and seek returns unrelated to benchmark exposures. Alternative assets – including real estate (especially value add/ opportunistic) – are usually classified as alpha drivers as they rely on complex, active strategies with a low correlation to traditional asset classes.

Beta, on the other hand, is a measure of systemic risk and can serve as a benchmark in the performance evaluation of an asset, fund or portfolio. Beta drivers are exposures to market risk factors and compensate for bearing non-diversifiable market risks.

Though they appear to be two separate concepts, alpha and beta can be seen as being on a spectrum. Alpha is intensely debated in academia and between professionals (especially with regard to the presence of “true alpha” and the ability to identify it). Moreover, alpha tends to become beta (or alternative beta) over time (source).

To provide a framework for the classification of investment skill, Schelling proposes a mechanism that not only aims to describe the nature and source of returns - identifying the manager’s ability to access this return stream and the probability of it continuing in the future - but that also presents investment skill as a spectrum. As the focus of this text is on real estate strategies in the context of value-add, the scope here is reduced to “manufactured alpha” (Schelling describes this as “hands-on alpha”) and “transitional alpha” (both deemed to be the most relevant in this context).

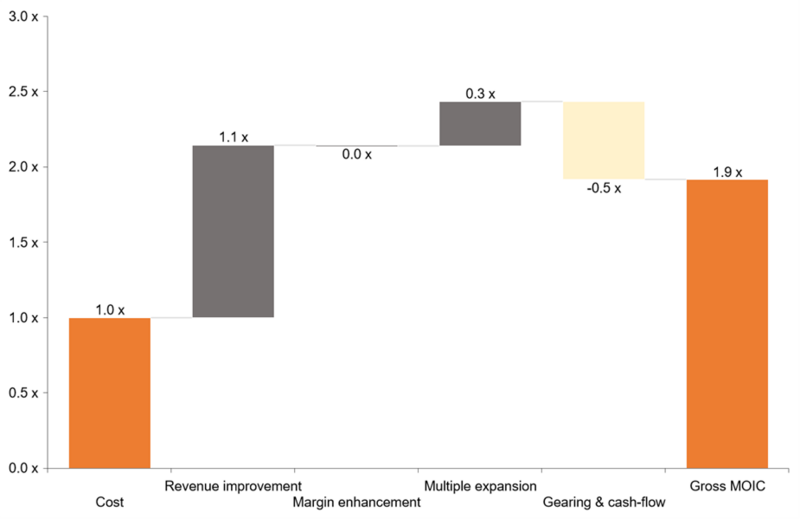

As presented above, we can see that the Gross MOIC (Multiple on Invested Capital) amounts to 1.9x after refurbishment and consideration of interim rental income. As the MOIC represents the multiple on the invested capital, this accounts for the equity share of total capex of 18.4% in addition to the initial equity employed (increasing the denominator). The amount of debt was assumed to keep a static debt to value ratio of 0.5x. Furthermore, an assumed distribution of interim cash-flows (i.e. NOI in T1 and T2 with 100% and 50% respectively) to the investor increases the nominator. We see that our equity increases 1.9-fold after refurbishment – with the debt-level remaining static. Yields go down, which was expected as we are developing to core. However, two main questions remain:

- What factors can the return be attributed to?

- What would be the impact be on a hypothetical portfolio of similar assets?

To answer the first question, we propose using a value bridge for performance and return attribution (see below), breaking down the relevant factors into the previously defined drivers: revenue improvement (e.g. via increased rent), margin enhancement (e.g. via leakage reduction), multiple expansion (e.g. via risk shift back to core) and gearing & cash-flow.

How to take the path to Net Zero carbon buildings

Net Zero White Paper

The exponential increase in anthropogenic greenhouse gas concentrations since industrialization is leading to an enhanced greenhouse effect. As a result, irreversible damage is being done to natural ecosystems and to our society. Based on this realization, the decarbonization approach has to become the focus of real estate development and construction.

Our research and the resulting decarbonization white paper provides you with all the necessary insights and information on this future-oriented and relevant topic. The data basis of the white paper consists of a broad portfolio study of 36 Implenia development projects based on SIA 2040, which was carried out in 2022.

Comments (0)

No comments found.